In this section we will deal with the Central banking system that operates in each account on the system. In each account, there is only one central banking account that operates from the Management level. When selecting an entity in the running of the relevant menu item, the entity will always be described as 'UM'

The principles applicable to the Central Trust Account will also apply to the Agent central banking system.

The central bank account is usually a trust account, and needs to be managed accordingly. In essence, there is one actual bank account, that is shared by many entities within the system. Every transaction, usually rental or levy receipts or payments to creditors, has to be allocated to an entity, or split among many entities, within the system (a Property, Agent or the Management level), and is also posted to a control account on the Management level.

At all times, the sum of the balances on the share of the trust account (General ledger account 3265) held by each participating entity, must equal the balance on the control account on the Management level (General ledger account 4155).

There is also usually a separate bank account, in which tenants deposits are held (4156). This account is generally only an investment type account, as very few transactions are usually processed through it each month. Tenant deposits and any refunds thereof are usually made from the central trust account (4155), and the total amounts thereof transferred as often as the transfer programs are run - Deposit in and Deposit out Clear, and Property Deposit Pay in / Pay out.

As with the share of the trust account (4155), the Deposit trust account is also a control account. All entries are processed to an individual entity (3266), and to the control account on the Management Level (4156). At all times, the sum of the balances on the share of the deposit trust account (General ledger account 3266) held by each participating entity, must equal the balance on the control account on the Management level (General ledger account 4156).

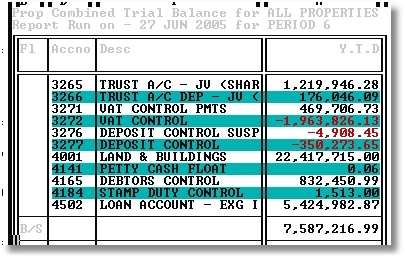

You will be able to view the current balances on the various accounts on a Management Level trial balance, an example of which is displayed below:

You will note that the balance on account 4155 is R 1 204 189. This is the amount that should be in the central bank account (The cash book balance for the accounting people) and represents the net Trust Creditors. .

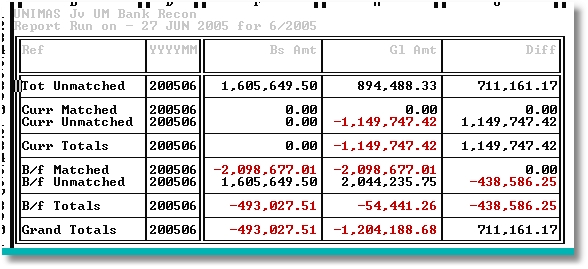

This balance is reconciled to the actual bank statement balance using the Bank Reconciliation facility on the Management Cash Book Menu. An example of the end part of the bank reconciliation is displayed below:

Note that the Total of the Gl column agrees with the balance on the trial balance. The balance per the bank statement is R 493 027, the difference being R 711 161, which difference is made up of the items in the 'Diff' column.

It is obviously critical to ensure that the reconciliation process in kept up to date, in order to ensure that the system record of the bank account is accurate.

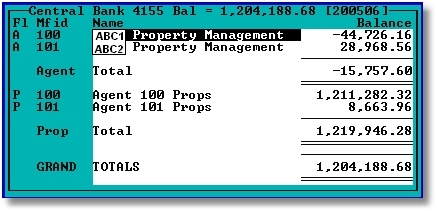

The amounts that make up the balance in the bank can be viewed using the report mentioned below. These amounts are usually referred to as trust creditors. Any negative amount would reflect amounts over drawn from the Trust account, which usually attract a lot of attention from trust account auditors.

The Central Bank Account Summary, on the Management Cash Book Menu will display all the balances as mentioned above. An example of this report is displayed below:

The above example is a summary report, with totals of all properties linked to the relevant agent. You could drill on the relevant figures to view the detail, or run the report choosing the 'F'ull option. It is a list of the balances on general ledger code 3265 for every property, every agent and the management level.

You will note that the balance on account 3213 on the above trial balance is the same as the balance on 4155 but in the negative. This is the contra account to accommodate the double entry accounting system, and serves no other purpose.

By monitoring the balances making up the trust account, and ensuring that the bank reconciliation is kept up to date, you should be in control of your trust account.

You should also cover the appropriate investment of the trust funds, which is not covered here.

In a similar way, the Deposit Trust can be managed and controlled.

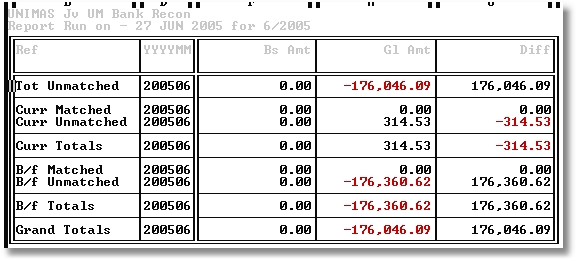

Note that the balance on account 4156 on the trial balance above is R 176 046. This is the amount that should be in the deposit trust current account. It should also be reconciled to the actual bank account using the same bank reconciliation facility as the one described above, except choosing 4156 instead of 4155. An example of the bank reconciliation is displayed below:

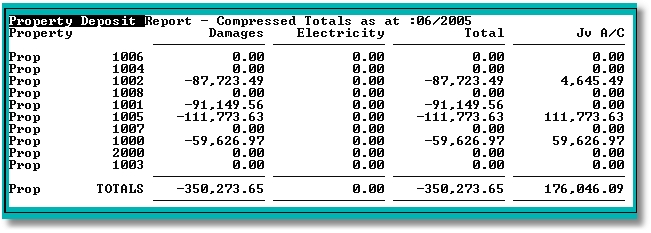

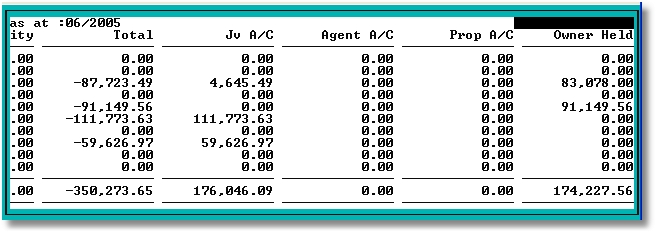

The balances making up the amount can be viewed using the Deposit Listing/Report on the Deposit Control Menu, an example of which is displayed below:

............

............

The two displays above represent one screen, separated for display purposes. The total of the JV A/C column is the amount that needs to balance to the bank account. The above displays were run using the Combined option, hence there is only one line per property. If run selecting the Full option, a detailed list of tenants and their deposits will be displayed per property.

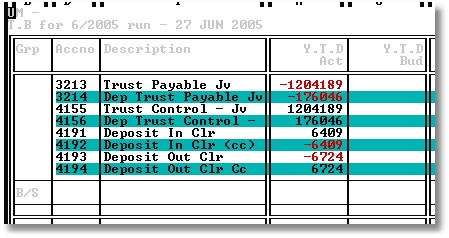

The following is a Combined Trial Balance of every property in the relevant account. You will note that the balance on account number 3266 (the sum of all properties' 3266) is the same as the deposit schedule and the trial balance.