In terms of the Sectional Title Schemes Management Act, all sectional title schemes are required to accumulate and maintain a reserve fund to be used to maintain the property, and provide for maintenance in the future. The old accumulated fund is now termed an administrative fund, which is separate from the reserve fund.

There is a formula in the act to determine the amount of the reserve fund, which fund is required to be invested in a separate bank account. There are various ways of achieving this from an accounting and control perspective. We have created a structure that will allow one property to contain both funds and manage the maintenance of the reserve fund bank account.

By using traditionally 'Balance Sheet' general ledger codes, this section of transactions is separated from the administration fund. The movement in these codes represents the income (levies and interest) and expenditure (maintenance and tax on interest) related to maintenance. The system income statements record this movement in a separate section, 'below the line'. There is also a financial year end process that transfers any surplus or shortfall for the financial year to a retained/carried forward reserve fund balance.

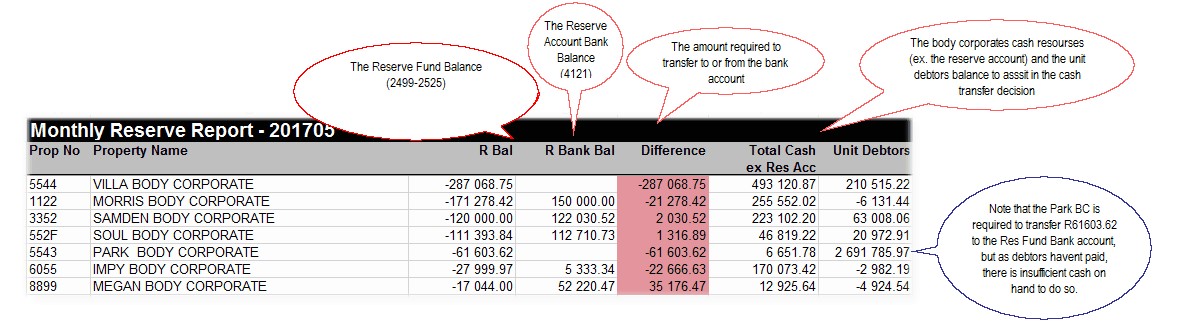

A key practice is too ensure that the reserve fund bank account is regularly 'synchronized' with the current reserve fund accounting balance. There are various factors to take into account in transferring funds to/from the reserve fund bank account , for eg. have all levies charged been paid. The system produces a summary report with all relevant information to enable you make informed transfer decisions.

The following sections contain key information and processes regarding the Reserve Fund/Account structure:

| Reserved General ledger codes |

A general ledger group for the reserve fund, RSA, is set up and all of the undermentioned codes are linked to it.

The general ledger codes used are:

|

||||||||||||||||||||||||

| The financial year end process for the Reserve Fund |

As with a normal accounting financial year end, the system allows for a reserve fund financial year end. As all of the general ledger codes used by the reserve fund are classical balance sheet codes, they are not impacted by the normal financial year end.

Choosing Reserve Accounts only by setting the flag to 'Y', will perform a financial year end on the reserve fund accounts. Leaving the flag blank or setting it to 'N', will perform the normal financial year end:

The process will transfer the net amounts as at the financial year end, for accounts 2500 to 2523, to 2499, which is the accumulated reserve fund over time.

|

A body corporate will decide on how much of its current accumulated fund should be transferred to the new Reserve Fund.

Once this decision is made, the amount decided on needs to be transferred from the accumulated fund, to the Reserve Fund (in the accounts) and to then effectively match this amount in the Reserve Fund bank account.

In order not to affect the income statement which should reflect the current movement only, the initial transfer to the Reserve Fund is usually processed, using general ledger journals, in two steps - 1. Transfer the relevant amount from the Accumulated Fund to a specific GL code (Usually 6990 - Trf. Acc. Fund to Reserve Fund) 2. Transfer the relevant amount to the reserve fund (2500) using 6991 (Transfer to Reserve fund)

This will trigger a cash movement to the Reserve Fund bank account as described below.

|

The reserve fund general ledger codes (except for 2499), have been added to the normal budget capture screen to allow the reserve fund budget to be captured.

|

This report is used as a control report and a cash movement initiation process to assist in ensuring that the balance of the reserve fund is matched with its bank account balance:

A system utility to build the required payment and receipt batches is being developed. |

The reserve fund movement is disclosed 'below the line' in the normal income statement:

|

The current balance of the reserve fund is disclosed under the Equity and Reserves as a separate line item.

The current reserve account bank account balance is included under Cash and Cash Equivalents.

A breakdown of the reserve account and the cash resources is included in the balance sheet notes:

|

The Financial Summary Report that is generally part of monthly client reporting, reports the Administrative and Reserve Funds as displayed in the image below:

|